While this article examines the unique and high-stakes environment of Ukraine, the fundamental principles of institutional investment discussed here apply universally across all transition and emerging economies. Whether a business operates in Eastern Europe, Latin America, or Southeast Asia, the core challenge remains identical: bridging the gap between local entrepreneurial success and the uncompromising compliance standards of global capital.

Introduction: The Paradox of Capital – Why the Market is Flush with Cash, Yet Your Business is Underfunded

In the fifth year of the full-scale war, the Ukrainian economy operates with unprecedented access to international capital. Despite colossal security challenges, the global financial architecture has transitioned from situational humanitarian aid to structured, systemic investment in the private sector. Today, billions of euros and dollars are accumulated in the market by key International Financial Institutions (IFIs) and private funds actively seeking investment targets. However, for many local entrepreneurs, this capital remains an unattainable mirage, creating the illusion of a closed market reserved exclusively for the “chosen few”.

The global capital market is undergoing a period of structural change. During the era of “cheap money,” investors often neglected deep due diligence in favor of deal speed. Today, however, the pendulum has swung back. Rising interest rates, geopolitical turbulence, and stringent compliance have transformed the M&A (Mergers and Acquisitions) landscape into a definitive “buyer’s market”.

As a Chief Financial Officer with years of hands-on experience in deal advisory, I regularly witness the same paradox. On one hand, billions are ready to enter the country. The European Bank for Reconstruction and Development (EBRD), the International Finance Corporation (IFC), and private players like Horizon Capital (with their €300 million Catalyst Fund) are actively scouting for investment targets. According to the “M&A Radar” report by KPMG, the volume of M&A deals in Ukraine grew by 20% in 2025 alone.

On the other hand, owners of local Small and Medium-sized Enterprises (SMEs) constantly face rejections. “We have a brilliant product, a 30% profit margin, and we are growing despite the war, but Fund X walked away after the first month of the audit. Why?” – this is the most common question I hear from CEOs.

The fundamental problem lies in the massive gap between Western capital’s expectations for transparency and the actual state of corporate governance and financial reporting within local companies. Investors do not deploy capital based on “word of honor” and management spreadsheets in Excel.

To understand the scale of missed opportunities, one must look at the current financing architecture. Global players offer a broad spectrum of capital-raising options: from direct equity and quasi-equity financing to classic debt lending, portfolio risk guarantees, and blended finance instruments. Today, specific programs with colossal budgets are already operational and ready to be deployed:

- Ukraine Facility (Pillar II): The Ukraine Investment Framework, with a budget of €9.5 billion, utilizes guarantees to mobilize up to €40 billion in private capital. Notably, a mandatory 15% quota is strictly reserved for lending to startups, micro, small, and medium-sized enterprises.

- Horizon Capital: The most powerful management company in the region, operating the $350 million Horizon Capital Growth Fund IV (primarily supporting tech and export-oriented enterprises). It has also launched the Horizon Capital Catalyst Fund with a target size of €300 million for projects in digital infrastructure, energy, and manufacturing. The Catalyst Fund aims to mobilize up to €3 billion for key sectors of the economy.

- Development Institutions (EBRD and IFC): The European Bank for Reconstruction and Development (EBRD) has specifically increased its capital by €4 billion and declares its readiness to invest approximately €1.5 billion annually, while the International Finance Corporation (IFC) portfolio in Ukraine has already reached $2.8 billion.

- Dragon Capital: Together with international partners, the firm has established the Amber Dragon Ukraine Infrastructure Fund I (target size of €350 million) and the Rebuild Ukraine Fund ($250 million) to finance recovery efforts (primarily targeting SMEs).

- Bilateral Government Funds (DFC, BII): The US International Development Finance Corporation (DFC) launched the URIF recovery fund with an initial capital of $150 million (primarily for equity investments), and the UK’s British International Investment (BII) allocated £250 million to support economic resilience.

These figures convincingly prove that there is no liquidity deficit in the market. The real bottleneck is an acute shortage of well-architected companies capable of withstanding the engineering stress test from auditors and meeting stringent transparency (compliance) criteria. Transforming your enterprise from a local business into a transparent institutional asset is the only key that unlocks the door to these resources. Therefore, the path to raising millions must begin not with seeking contacts at foreign funds, but with a comprehensive redesign and overhaul of your own financial foundation. фундамента.

In this article, I will break down the anatomy of Financial Due Diligence step by step. We will discuss what Western investors are actually looking at, why shadow cash flows destroy valuation multiples, and how a modern CFO acts as the architect capable of streamlining a company and transforming it into an institutionally mature asset.

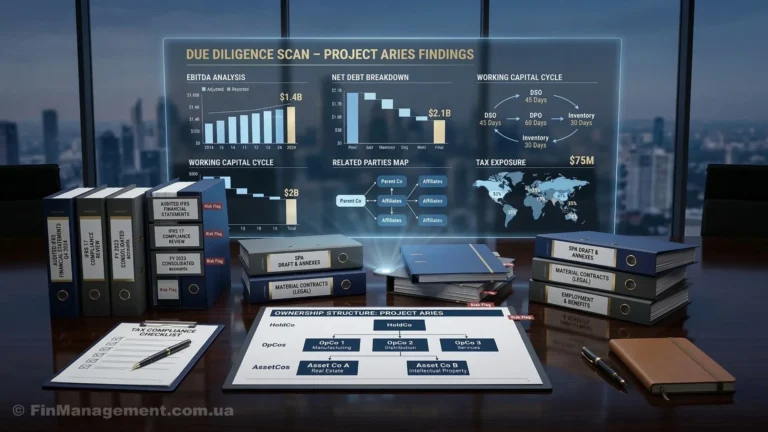

The Anatomy of Financial Due Diligence: More Than Just an Audit

Many entrepreneurs mistakenly believe that if their company undergoes a mandatory statutory audit every year and has no issues with the tax authorities, it is ready for an investor to step in. There is a conceptual chasm between a standard audit and a Due Diligence (DD) procedure.

A standard audit simply confirms that your financial statements are prepared without material misstatements. Financial Due Diligence (FDD) is a deep investigation aimed at identifying “kill switches” (value-destroying mechanisms). The investor and their appointed advisors (often from the “Big Four” – EY, PwC, KPMG, Deloitte) are looking for the answer to one core question: does this company actually generate the claimed cash flow, and what hidden landmines might explode after the deal is signed?

Every discrepancy found (for example, unrecorded accrued vacations) is not merely documented in a report – it is directly deducted from the Valuation you will receive in hand.

The architecture of a modern, comprehensive due diligence process rests on several pillars:

- Financial Block (Quality of Earnings & Net Debt): This is the heart of the review. Auditors calculate your normalized EBITDA, ruthlessly stripping out one-off revenues, subsidies, or income from non-core assets. They analyze your Working Capital requirements and, most importantly, calculate your Net Debt, which will include not only bank loans but also hidden liabilities (e.g., accumulated vacation pay or overdue taxes).

- Tax Block (Tax Due Diligence): The search for historical tax sins. The statute of limitations in Ukraine is 3 years (and 7 years for transfer pricing). Any questionable transactions with counterparties will be identified and quantified as a potential penalty, which the buyer will directly deduct from the deal value.

- Legal Block (Legal DD): Verification of the “cleanliness” of rights to key assets. If the source code of your IT startup belongs to a freelance contractor (sole proprietor) rather than the company, there will be no deal.

- Compliance and ESG: Today, this is a mandatory filter. Investors screen against sanctions lists, check AML (Anti-Money Laundering) procedures, and verify compliance with environmental and social standards. As a PwC investor survey shows, over 80% of financial institutions now explicitly integrate ESG metrics into their strategies and decision-making processes.

Dismantling “Grey” Schemes: From Temporary Structures to Institutional Transparency

Historically, local businesses have grown in an environment of aggressive tax planning. The practice of keeping two sets of books – a “white” one for the tax authorities and a “management” one for the owner – was the norm. However, for a Western institutional investor, this is an absolute deal-breaker. Western institutional capital has zero tolerance for dual accounting and any opaque operational mechanisms, as strict internal compliance rules dictated by US or EU regulators categorically prohibit investing in assets with unverified origins of capital.

Deconstructing Optimization “Crutches”

During the preparation phase, the first thing an experienced CFO does is deconstruct the internal optimization mechanisms that investors perceive as Red Flags.

- Artificial Fragmentation via Sole Proprietorships (FOPs): This is a classic SME setup – using dozens of individual entrepreneurs to minimize taxes. For an investor, this is a catastrophic risk. First, there is the threat of reclassifying civil law contracts into employment relations (resulting in massive fines). Second, it destroys the ability to verify the true Cost of Goods Sold (COGS), as inventory accounting is often fragmented. Poland went through a similar journey: any attempt to sell a business operating as a sole proprietorship is blocked right at the start, requiring prior transformation into a corporate entity.

- Transfer Pricing and Offshore Shells: Tax authorities (both locally and in the EU) strictly apply the Business Purpose Test. The use of complex corporate structures or offshore shell companies without clear economic substance is guaranteed to derail negotiations. Today, any convoluted ownership structure is viewed through the lens of Anti-Money Laundering (AML) risks; therefore, hidden beneficiaries or opaque cross-border payments instantly kill investments.

- Refundable Financial Assistance (Owner Loans): Financing a business through continuous “interest-free loans” from the owner. For auditors, this is a glaring marker that the business is incapable of generating sufficient cash flow to cover its Working Capital needs.

What Should the Corporate Architecture Look Like?

To become “investable”, a business must be consolidated into a single corporate perimeter – a transparent holding structure (SPV). Within this revamped architecture, operational activities (OpCo) and high-value asset holding centers (AssetCo) must be logically separated but legally connected by arm’s length market contracts.

The investor needs to see a functional Board of Directors, not a company managed “manually” via instant messengers.

This transformation relies on the principles of institutional maturity, which are reflected in modern transparent business standards and exactly mirror the requirements of Western funds:

- A complete absence of tax debt and social security contribution arrears.

- Absolute transparency regarding Ultimate Beneficial Owners (UBOs) with zero sanctions footprint.

- A clean VAT history and an impeccable counterparty track record.

- Strict adherence to currency control regulations, specifically settlement deadlines for export-import operations.

IFRS: The Universal Language of Investor Communication

One of the most painful stages of preparation is the conversion of financial statements. If you bring financial statements based on Ukrainian National Accounting Standards (UAS) to a Western fund, you simply will not be understood.

International Financial Reporting Standards (IFRS) are the global Esperanto of business. They allow a fund from London or Warsaw to accurately compare your profitability with a manufacturing plant in Germany.

The problem is that for decades, local accounting has been subordinated exclusively to fiscal goals (calculating the tax base). IFRS, on the other hand, is built on the fundamental principle of “substance over form”.

How Does IFRS Change Your Valuation (EBITDA) During DD?

Owners are often surprised when, after the transformation of financial statements, their “beautiful” EBITDA shrinks or, conversely, unexpectedly grows. Let’s look at the key differences:

- Lease Accounting (IFRS 16): Under local standards, office rent is treated merely as a monthly expense. Under IFRS, most long-term lease agreements are capitalized: you must recognize a Right-of-Use (RoU) asset and a corresponding lease liability on the balance sheet. As a result, lease payments disappear from operating expenses (turning into depreciation and interest), which artificially inflates your EBITDA. But simultaneously, this increases your Net Debt. The investor knows this and adjusts their models accordingly.

- Impairment of Assets (IFRS 9 / IAS 36): SMEs in transition economies almost never impair bad debts to avoid showing losses. IFRS requires the recognition of provisions for Expected Credit Losses (ECL). This protects the investor from inflated balance sheets.

- Revenue Recognition (IFRS 15): Locally, revenue is often tied to the signing of a “certificate of completion” (driven by VAT rules). IFRS recognizes revenue when the customer obtains control of the asset or service, which reflects real cash flows much more accurately.

A Practical Solution From the CFO

For mid-sized businesses, maintaining Full IFRS is too expensive. The ideal compromise is implementing IFRS for SMEs. This standard reduces disclosure requirements by roughly 90% but completely satisfies institutional investors.

A detailed review of IFRS for SMEs will help you understand the conceptual differences: [Link to your article]

An important strategic caveat: Choose the standard based on your ultimate goal. IFRS for SMEs is perfect for classic private capital raising or bank lending. However, if your long-term horizon includes an IPO or attracting top-tier global equity funds, initiate the transition from local GAAP directly to Full IFRS. Using the SME standard as an intermediate step is impractical – it will lead to double work for your finance department and unjustified transformation costs.

You can use my [IFRS Reference Guide] as a working tool for this transit.

An important nuance that is often overlooked: local legislation allows companies to voluntarily switch to IFRS and completely abandon National Accounting Standards. Depending on the business’s readiness for change, CFOs typically choose one of three approaches for the technical implementation of this transition:

- Manual Transformation: Transferring local accounting data into the IFRS format at the end of the reporting period via manual adjustments (often in Excel). This is a classic “crutch” (a dangerous workaround) – a temporary solution that seems cheapest at the start, but is highly risky due to extreme subjectivity and the likelihood of critical errors.

- Automated Translation / Mapping (ERP Integration): Configuring modern ERP systems where the company continues to operate within the local GAAP paradigm, but every primary transaction is automatically duplicated according to IFRS rules. This ensures accuracy and regularity but requires complex setup and the constant maintenance of a dual methodology.

- Full IFRS Transition (Systemic Solution): Officially changing the accounting policy and maintaining a single primary ledger in the ERP exclusively according to international standards. Tax accounting then relies on the IFRS financial result, applying statutory tax differences.

As a financial architect, I strongly recommend moving away from the manual transformation of financial statements. The optimal systemic solution is a complete, legal abandonment of local standards in favor of a single IFRS-based ledger. However, if the company lacks the infrastructure for this, the best alternative is to implement automated transaction mapping at the architectural level of your ERP system.

Balance Sheet Clean-Up: Getting Rid of Toxic Assets

No sound fund will buy a company whose balance sheet resembles a graveyard of illiquid assets and doubtful debts. Balance Sheet Clean-up is a critical task for a CFO at least a year before negotiations begin.

1. Managing Non-Performing Loans (NPLs) Due to the war, many companies have accumulated dead receivables from counterparties that ended up in occupied territories or went bankrupt. Keeping them on the balance sheet means distorting liquidity ratios. Solution: A strict Write-off or the sale of the distressed debt pool to factoring companies at a discount. This will take a one-time toll on the financial result, but it will fundamentally heal the capital structure.

2. Spin-Off of Non-Core Assets Successful local businesses have historically accumulated everything: from “employee” recreation centers to “just in case” land plots and corporate yachts. A Western fund looking to invest in your agritech platform does not want to buy your resort in the Carpathians. It does not want to bear the associated legal risks. Solution: The CFO executes a Spin-off – legally and financially carving out the core business (OpCo) into a separate, clean structure that the investor actually buys. All non-core and risky assets remain outside the transaction perimeter under the founders’ ownership (AssetCo).

3. Related Party Transactions If you sell raw materials to your brother’s company at below-market prices, an auditor during FDD will view this as a hidden capital extraction. To successfully pass Financial Due Diligence, the business system architect (CFO) must ensure the following clean-up criteria are met:

- Transition all procurement, leasing, and service operations between affiliated entities strictly to a commercial basis, adhering to the Arm’s Length Principle.

- Fully restructure, settle via offset, or repay historical intercompany debts before active negotiations with the fund begin.

- Convert “toxic” debt owed to founders into equity (debt capitalization) if the company lacks sufficient liquidity to repay it in cash.

Executing such an uncompromising “spring cleaning” allows for reducing the overall estimated transaction value to a level adequate for the fund, while simultaneously isolating the core business from hidden historical threats. Only a highly liquid, cleaned-up balance sheet with no financial black holes or non-operating “garbage” can convince an investor of your institutional maturity.

Emergency Indicators: “Red Flags” That Destroy Deals

An analysis of failed deals points to specific triggers after which investors simply close their laptops and walk away.

- Sanctions Compliance and AML (Anti-Money Laundering): Geopolitics has changed everything. If there are counterparties linked to sanctioned countries in your supply chain (even through third countries), it is a death sentence for the deal. High-profile scandals involving the Baltic branches of Nordea and Danske Bank, which paid hundreds of millions in fines for money laundering, have taught European business a hard lesson: KYC (Know Your Customer) is not a mere formality.

- Russian or Belarusian Footprint: Even the presence of 1% of Russian capital somewhere at the level of minority founders in an offshore structure makes an investment in a Ukrainian company impossible due to sanctions legislation.

- Cybersecurity and IT “Kill Switch”: This is particularly relevant for tech deals. The investor cares not only about the technical execution of the product but also about the management background: your true motives, adequate risk assessment, and the existence of a clear “Plan B” in case of failure (“Intent, Fear, Kill Switch”). If it turns out that user databases are not encrypted (an EU GDPR violation) or you are using pirated software, the startup’s valuation drops to zero.

- Ignoring ESG: Over 80% of financial investors integrate ESG metrics into their strategies. Workplace safety, environmental control, and corporate governance are now a mandate. Horizon Capital, for example, strictly requires compliance with environmental and gender policies right at the due diligence stage.

The Anatomy of Failures and Successes in Ukraine

The most striking example of a catastrophic Due Diligence is the privatization story of the Odesa Port Plant (OPZ). Despite its unique potential, the audit consistently revealed colossal debt obligations (including $250 million owed to Firtash’s structures), a trail of corruption, and security risks. Investors could not overcome internal compliance barriers, and the asset’s value plummeted significantly.

In contrast, the Ukrainian IT company HOLYWATER (an AI startup) successfully raised $22 million from Horizon Capital. They passed the most rigorous audit by EY, proving the flawlessness of their databases, intellectual property protection, and the transparency of financial metrics according to international standards. Another example is the pharmaceutical giant Farmak, which fully digitized its Third-Party Risk Management (TPRM) processes by replacing old Russian software with the local low-code platform Nectain, ensuring instant sanctions screening and readiness for audits.

A CFO’s Preparation Roadmap

The root cause of most failed transactions lies in flawed timing: owners begin preparing for an audit only when the investor is already at the doorstep. Under severe time constraints, the Chief Financial Officer (CFO) physically lacks the time to restructure debts, consolidate assets, and transition accounting to international standards. This leads to information asymmetry, which always works against the seller during the review.

To avoid falling victim to “information asymmetry” (where the buyer’s auditors find your weak spots and use them to aggressively drive down the price), the company must act proactively.

This tool is called Vendor Due Diligence (VDD) – an independent comprehensive audit initiated and paid for by the seller well in advance of meeting with investors.

As a CFO, I structure the preparation process into two phases:

Phase 1: Strategic Restructuring (12–24 Months Before the Deal)

- Diagnostics: Hiring independent consultants for a rigorous crash test of internal accounting, taxes, and legal structure. We look for our own “Red Flags” before external analysts see them.

- Corporate Restructuring: Transitioning from a fragmented model (using sole proprietorships) to a transparent holding structure. Consolidating key tangible assets and intellectual property within a single, protected corporate perimeter.

- IFRS Project: Launching the transition of financial reporting to IFRS for SMEs. Selecting a new accounting policy.

An excellent practical example of such proactive and systemic preparation is the experience of the Ukrainian pharmaceutical company Farmak. Preparing for rigorous international audits, the company completely abandoned risky Russian software in favor of the modern low-code platform Nectain to automate its internal Vendor Due Diligence. By implementing end-to-end counterparty verification via YouControl (sanctions screening) and ensuring complete document traceability, the company minimized compliance risks and fulfilled the mandatory conditions for exporting to over 50 countries worldwide. Another benchmark is the tech company HOLYWATER, which, thanks to a flawless database architecture, protected intellectual property, and transparent financial metrics, successfully passed a comprehensive audit by EY and raised $22 million from the Horizon Capital fund.

Phase 2: Operational Systematization (6–12 Months Before the Deal)

- Fast Closing: Configuring the ERP system so that management reporting is ready by the 10th of every month without fail. Delays with numbers instantly trigger distrust from funds.

- Balance Sheet Clean-Up: Completing the write-off of bad debt and the separation of AssetCo.

- Virtual Data Room (VDR): Creating a secure cloud repository where all documentation, contracts, licenses, and audit reports for the last three years are organized into folders according to international standards. When the investor says, “We are ready to start DD,” we grant them access to the room within 24 hours, demonstrating total control over the business.

The CFO’s ability to execute this two-year transformation plan turns the company from a local, founder-dependent enterprise into a highly liquid asset ready for scaling. Such strategic preparation unconditionally proves the institutional maturity of the business, preempts the vast majority of questions from investment committees, and allows for defending the maximum Valuation of the company. Ultimately, it is this systemic approach that guarantees the multi-month Financial Due Diligence will end not with broken negotiations, but with capital successfully flowing into your business’s accounts.

Summary: Institutional Maturity as the Ultimate Capital

Raising financing in 2026 is not a matter of networking or flashy presentations. It is a matter of systemic, institutional maturity. Financial Due Diligence is a stress test of your business model’s viability.

The transition from “manual” management and tax optimization to a transparent international structure requires time (up to 2 years), significant investments, and a shift in the founders’ mindset. However, it is exactly this transformation that turns the company from a local business into a highly liquid asset. The role of a modern CFO is precisely to be the architect of this transformation, guiding the company through the “valley of death” of the audit and opening the doors to multi-million investments.

If your business is ready to scale, start building your investment equity story today.

Rapid Diagnostics: 5 Uncomfortable Questions for the Business Owner

Before initiating the capital-raising process or entering negotiations with investment funds, give an honest answer to these five questions:

- Transparency Architecture: If tomorrow the fund’s auditors ask for a consolidated EBITDA figure for the last 3 years, how many weeks will it take your finance department to “compile” the data from dozens of sole proprietorships (FOPs), related companies, and management spreadsheets?

- Valuation Impact: Do you know today by how many millions of dollars your company’s valuation will drop after auditors deduct non-market internal transactions from the profit and normalize the working capital?

- IFRS as an Indicator: Does your finance department understand exactly how lease capitalization (IFRS 16) or impairment testing (IAS 36) will change your balance sheet structure, and what the investor will see in these new numbers?

- Legal Perimeter (Kill Switch): Do all key assets legally belong to the companies included in the Transaction Perimeter, or does a part of your business still operate on unregistered intellectual property and equipment rented from relatives?

- Operational Resilience: Is your finance department capable of processing an Initial Request List from auditors consisting of 200+ items (with scans of all contracts, breakdowns of normalized EBITDA, and the structure of capital expenditures for 3 years) within 5 days, and then withstanding continuous rounds of Q&A without halting current payments and operational business management?

If you answered “no” or “I don’t know” to at least two of these questions, your company needs time for preparation (Vendor Due Diligence) and an architectural overhaul of the finance function before opening the doors to investors.