This article is a comprehensive guide to the 2018 Conceptual Framework for CFOs and auditors. We break down the changes in asset definitions and the new recognition criteria.

1. Introduction: Status and Purpose of the Conceptual Framework

The Conceptual Framework for Financial Reporting is a fundamental document issued by the International Accounting Standards Board (IASB) that sets out the objectives and concepts underlying general purpose financial reporting. Its strategic importance lies in serving as the intellectual foundation for the development of consistent and logically sound standards. This ensures a unified approach and facilitates the high-quality interpretation of financial information by all stakeholders.

It is crucial to clearly distinguish the status of the Conceptual Framework from the IFRS Standards themselves. As stated in paragraph SP1.2, the Conceptual Framework is not a Standard, and nothing in it overrides any specific Standard or its requirements. Furthermore, as explained in paragraph SP1.3, to meet the general objective of financial reporting, the IASB may explicitly set requirements that depart from aspects of the Conceptual Framework. In such cases, the Board explains the rationale for the departure in the “Basis for Conclusions” of the relevant Standard, demonstrating a pragmatic approach to standardization.

According to paragraph SP1.1, the Conceptual Framework has three key objectives that define its practical significance:

- Assisting the IASB: To provide a consistent conceptual basis for developing new Standards and revising existing ones. This ensures the logical coherence and consistency of the IFRS system.

- Assisting Preparers: To facilitate the development of consistent accounting policies when no Standard applies to a particular transaction, or when a Standard allows a choice of accounting policies.

- Assisting All Parties: To aid in understanding and interpreting the Standards by revealing the logic underlying their requirements.

Synthesizing the global mission of the IFRS Foundation, the Conceptual Framework (paragraph SP1.5) contributes significantly to the functioning of global financial markets. It enhances transparency by improving international comparability and the quality of financial information. This, in turn, strengthens accountability by providing investors and other capital providers with the information needed to hold management to account. Consequently, economic efficiency increases, as high-quality information helps investors identify risks and opportunities, fostering better capital allocation in the global economy.

Thus, the Conceptual Framework lays the theoretical foundation from which the primary objective of financial reporting itself is derived.

2. Objective of General Purpose Financial Reporting

The objective of financial reporting is the cornerstone of the entire Conceptual Framework. All other aspects flow logically from it: from the qualitative characteristics of information to the principles of recognition and measurement of elements. Clearly defining this objective is critical, as it determines what information is useful, for whom it is intended, and what decisions it supports.

According to paragraph 1.2, the objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders, and other creditors in making decisions relating to providing resources to the entity. These decisions involve buying, selling, or holding equity and debt instruments, as well as providing or settling loans. It is important to note that these groups are identified as primary users because they must rely on general purpose financial reports for much of the financial information they need (paragraph 1.5).

To make informed decisions, these primary users require specific information (paragraphs 1.3 and 1.4) that allows them to assess the prospects for the entity’s future net cash inflows. This need is detailed in the following aspects:

- Information on Economic Resources and Claims. Data on the company’s assets and liabilities help users identify its financial strengths and weaknesses, assess liquidity and solvency, and evaluate needs for additional financing.

- Information on Changes in Economic Resources and Claims. It is essential for users to understand the reasons for these changes. Specifically, to distinguish changes resulting from financial performance from changes caused by other events (e.g., issuing new shares or obtaining loans).

- Information on Management Stewardship. Financial reporting should reflect how effectively and efficiently management has discharged its responsibilities regarding the use of the entity’s economic resources. This reflects the concept of stewardship, highlighting the dual role of reporting: providing information for investment decisions and for assessing how management has utilized the resources entrusted to it.

A key role in providing such information is played by accrual accounting (paragraph 1.17). Unlike the cash basis, which records only cash movements, accrual accounting depicts the effects of transactions and other events in the periods in which they occur, even if the resulting cash receipts and payments occur in a different period. This provides a significantly better basis for assessing the entity’s past and future financial performance.

At the same time, it is important to recognize the limitations of financial reporting. According to paragraphs 1.6 and 1.7, general purpose financial reports do not and cannot provide all the information that users need; users must also consider general economic conditions, industry and political risks. Furthermore, financial reports are not designed to show the value of a reporting entity; but they provide information to help users estimate the value of the reporting entity.

To achieve its objective and provide useful information, financial data must possess certain qualitative characteristics.

3. Qualitative Characteristics of Useful Financial Information

Qualitative characteristics are the attributes that make financial information useful to users. They serve as criteria for assessing the quality of data presented in financial reports. These characteristics are divided into two categories: fundamental, which are mandatory, and enhancing, which improve the utility of the information.

3.1. Fundamental Qualitative Characteristics

The fundamental qualitative characteristics are relevance and faithful representation. Information must possess both qualities to be useful.

Relevance

Information is relevant if it is capable of making a difference in the decisions made by users (paragraph 2.6). It has either predictive value, confirmatory value, or both.

- Predictive value (paragraphs 2.7–2.8) means the information can be used as an input to processes employed by users to predict future outcomes. For example, revenue data for the current year can serve as a basis for forecasting revenue in future periods.

- Confirmatory value (paragraph 2.9) means the information provides feedback about previous evaluations—confirming or changing them. For instance, the same revenue report for the current year allows users to compare actual results with previously made forecasts.

An essential aspect of relevance is Materiality. According to paragraph 2.11, information is material if omitting, misstating, or obscuring it could reasonably be expected to influence decisions that the primary users make. Materiality is an entity-specific aspect of relevance based on the nature or magnitude (or both) of the items to which the information relates in the context of an individual entity’s financial report.

Faithful Representation

Financial reports represent economic phenomena in words and numbers. To be useful, financial information must not only represent relevant phenomena but also faithfully represent the substance of the phenomena that it purports to represent—their economic substance, not merely their legal form (paragraph 2.12). A perfectly faithful representation would have three characteristics (paragraphs 2.13–2.19):

- Completeness: Inclusion of all information necessary for a user to understand the phenomenon being depicted, including all necessary descriptions and explanations.

- Neutrality: The selection or presentation of financial information is without bias. Neutrality is supported by the exercise of prudence, which is the exercise of caution when making judgments under conditions of uncertainty. This means that assets and income are not overstated and liabilities and expenses are not understated. However, according to paragraph 2.17, prudence does not imply a need for asymmetry, such as a systematic need for more persuasive evidence to support the recognition of assets or income than the recognition of liabilities or expenses. Such asymmetry is not a qualitative characteristic of useful financial information.

- Free from error: This does not mean perfect accuracy in all respects. It means there are no errors or omissions in the description of the phenomenon, and the process used to produce the reported information has been selected and applied with no errors in the process. The use of reasonable estimates is an essential part of the preparation of financial information and does not undermine faithful representation if the nature and limitations of the estimation process are described clearly and accurately.

3.2. Enhancing Qualitative Characteristics

These characteristics enhance the usefulness of information that is already relevant and faithfully represented. They also help determine which of two ways should be used to depict a phenomenon if both are considered equally relevant and faithfully represented.

Table 3: Enhancing Qualitative Characteristics

| Characteristic | Analysis of Meaning and Impact |

|---|---|

| Comparability | Enables users to identify and understand similarities in, and differences among, items both across different entities and within the same entity for different periods (paragraphs 2.24–2.25). Comparability is not uniformity; conversely, for information to be comparable, like things must look alike and different things must look different. Consistency refers to the use of the same methods for the same items, which helps to achieve comparability but is not the same as comparability (paragraph 2.26). |

| Verifiability | Helps assure users that information faithfully represents the economic phenomena it purports to represent (paragraph 2.30). It means that different knowledgeable and independent observers could reach a consensus, although not necessarily complete agreement, that a particular depiction is a faithful representation. Verification can be direct (e.g., counting cash) or indirect (checking the inputs to a model and recalculating the output) (paragraph 2.31). |

| Timeliness | Means having information available to decision-makers in time to be capable of influencing their decisions (paragraph 2.33). Generally, the older the information is, the less useful it is, although some information (e.g., for trend analysis) may continue to be timely for a long time. |

| Understandability | Classifying, characterizing, and presenting information clearly and concisely makes it understandable (paragraph 2.34). This presumes that users have a reasonable knowledge of business and economic activities. However, it does not mean that complex information should be excluded from financial reports solely because it may be too difficult for some users to understand, as this would make the reports incomplete and potentially misleading (paragraph 2.35). |

3.3. The Cost Constraint

Cost is a pervasive constraint on the information that can be provided by financial reporting (paragraphs 2.39–2.43). Reporting financial information imposes costs, and it is important that those costs are justified by the benefits of reporting that information. The IASB and preparers must constantly balance these two aspects to ensure the maximum utility of reporting within reasonable costs.

These qualitative characteristics apply to all information presented in the financial statements, the concept of which is discussed next.

4. Financial Statements and the Reporting Entity

Financial statements are the primary means of communicating financial information about an entity’s economic resources, claims, and changes in them. This section of the Conceptual Framework outlines the scope, key assumptions, and boundaries of reporting.

According to paragraphs 3.2–3.3, the objective and scope of financial statements is to provide information about assets, liabilities, equity, income, and expenses. This information is provided in the following forms:

- Statement of financial position, which recognizes assets, liabilities, and equity.

- Statement(s) of financial performance, which recognizes income and expenses.

- Other statements and notes, which present and disclose detailed information about recognized and unrecognized elements, cash flows, contributions from holders of equity claims, and accounting policies applied.

Fundamental to the preparation of financial statements are the concepts of the reporting period (paragraphs 3.4–3.5)—the specific period of time covered by the statements—and the going concern assumption (paragraph 3.9). The latter implies that financial statements are prepared on the assumption that the reporting entity is a going concern and will continue in operation for the foreseeable future, having neither the intention nor the necessity of liquidation. If this assumption is not appropriate, the financial statements may need to be prepared on a different basis, which must be disclosed.

A central concept is the reporting entity (paragraphs 3.10–3.14). This is an entity that is required, or chooses, to prepare financial statements. Importantly, a reporting entity is not necessarily a legal entity; it can comprise a portion of an entity or comprise more than one entity. The boundaries of such an entity are determined by the information needs of the primary users for relevant and faithfully represented information.

It is this extension of the reporting entity concept beyond a single legal entity that provides the theoretical basis for distinguishing between consolidated and unconsolidated financial statements (paragraphs 3.15–3.18):

- Consolidated financial statements provide information about a parent and its subsidiaries as a single reporting entity. They are crucial for assessing the prospects of the group as a whole, as they address economic resources and claims under common control.

- Unconsolidated financial statements provide information about the parent alone as a separate legal entity. While they may be useful to the parent’s specific creditors, they are not a substitute for consolidated financial statements, as they do not provide a complete view of the group’s resources and performance.

Financial statements, in turn, consist of specific elements, the definition of which is the next key step in the analysis.

5. Elements of Financial Statements

The elements of financial statements are the building blocks that constitute financial reports. They are classified into two main groups: elements representing financial position at a specific date (assets, liabilities, equity), and elements representing financial performance for a period (income and expenses). The relationship of these elements to economic resources and claims is shown in the table below, which reproduces the structure of Table 4.1 of the Conceptual Framework.

Table 5: Elements of Financial Statements

| Item | Element | Definition or Description |

|---|---|---|

| Economic resource | Asset | A present economic resource controlled by the entity as a result of past events. An economic resource is a right that has the potential to produce economic benefits. |

| Claim | Liability | A present obligation of the entity to transfer an economic resource as a result of past events. |

| Equity | The residual interest in the assets of the entity after deducting all its liabilities. | |

| Changes in economic resources and claims reflecting financial performance | Income | Increases in assets, or decreases in liabilities, that result in increases in equity, other than those relating to contributions from holders of equity claims. |

| Expenses | Decreases in assets, or increases in liabilities, that result in decreases in equity, other than those relating to distributions to holders of equity claims. | |

| Other changes in economic resources and claims | Contributions from holders of equity claims and distributions to them. Exchanges of assets or liabilities that do not result in increases or decreases in equity. |

5.1. Analysis of the Elements of Financial Position

Asset

According to the definition (paragraph 4.3), an asset is a present economic resource controlled by the entity as a result of past events. This definition includes three key aspects:

- Right: This can be a right to receive cash, goods, or services, or a right to use physical objects (paragraphs 4.6–4.13). Crucially, the right must already exist.

- Potential to produce economic benefits: The right has the potential to produce economic benefits. It is not necessary for the benefits to be certain or even likely; it is sufficient that the potential exists in at least one circumstance (paragraphs 4.14–4.18).

- Control: An entity controls an economic resource if it has the present ability to direct the use of the economic resource and obtain the economic benefits that may flow from it, while also restricting the access of others to those benefits (paragraphs 4.19–4.25). It is important to emphasize that control is based on present ability, which may arise from legal rights or other means (e.g., control over “know-how”), and does not always coincide with legal ownership (paragraph 4.22).

Liability

According to the definition (paragraph 4.26), a liability is a present obligation of the entity to transfer an economic resource as a result of past events. The existence of a liability is determined by three criteria:

- Obligation: This is a duty or responsibility that the entity has no practical ability to avoid. An obligation can be legal (enforceable by contract or law) or constructive (arising from established business practices, published policies, or specific statements) (paragraphs 4.28–4.35).

- Transfer of an economic resource: The obligation must have the potential to require the transfer of an economic resource (e.g., cash, goods, services). Even a low probability of transfer does not negate the existence of the obligation (paragraphs 4.36–4.41).

- Present obligation as a result of past events: The obligation exists now because the entity has already obtained economic benefits or taken action in the past that will require it to transfer an economic resource in the future (paragraphs 4.42–4.47).

Equity

Equity is residual in nature. It is the residual interest in the assets of the entity after deducting all its liabilities (paragraph 4.63). It represents the claims of owners against the net assets of the company.

5.2. Analysis of the Elements of Financial Performance

Income

Income is increases in assets, or decreases in liabilities, that result in increases in equity, other than those relating to contributions from holders of equity claims (paragraph 4.68).

Expenses

Expenses are decreases in assets, or increases in liabilities, that result in decreases in equity, other than those relating to distributions to holders of equity claims (e.g., dividend payments) (paragraph 4.69).

Having defined the elements, the logical question arises: under what conditions should these elements be included in the financial statements?

6. Recognition and Derecognition of Elements

Recognition is the process of capturing for inclusion in the statement of financial position or the statement of financial performance an item that meets the definition of one of the elements—an asset, a liability, equity, income, or expenses. This section of the Conceptual Framework establishes the criteria that determine exactly when an element should be reported.

6.1. The Recognition Process and Criteria

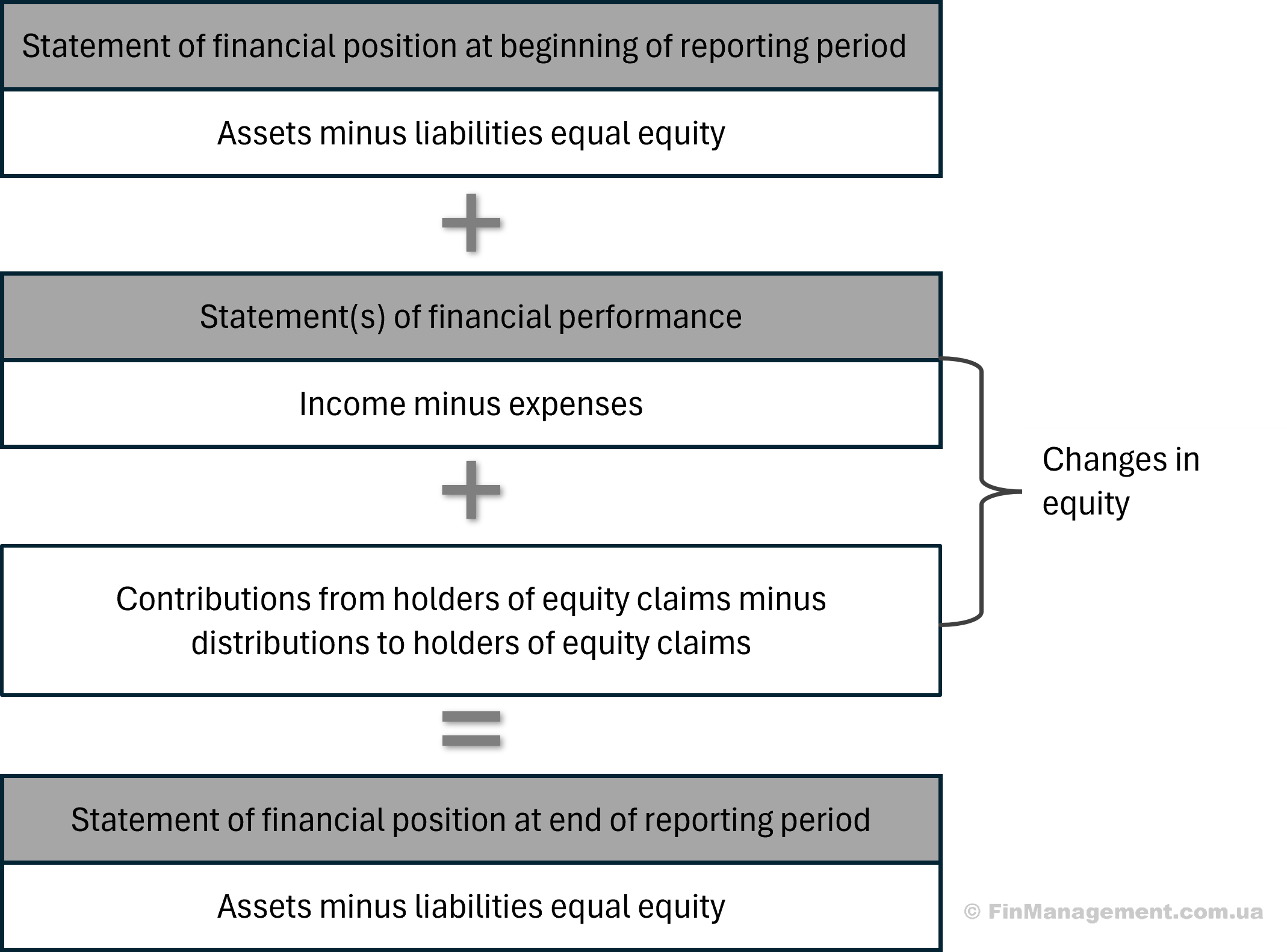

The recognition process acts as the integral link between the statement of financial position and the statement of financial performance (paragraphs 5.1–5.5). This fundamental relationship, which underpins the double-entry system, is visualized in Diagram 5.1 of the Conceptual Framework:

This scheme illustrates that the recognition of one item inevitably requires the recognition or change of another. For example, the recognition of income from the sale of goods occurs simultaneously with the increase of an asset (cash or accounts receivable) and the derecognition of another asset (inventory), which leads to the recognition of an expense.

An asset or liability is recognized only if recognizing it provides users with useful information. According to paragraph 5.7, this occurs provided that two main criteria are met, which can be formulated as answers to two key questions:

- Does recognition provide relevant information? Information may not be relevant if there is significant existence uncertainty regarding the asset or liability, or if the probability of an inflow or outflow of economic benefits is low. In such cases, recognition may not provide useful information, and disclosure in the notes may be more appropriate.

- Does recognition provide a faithful representation? Even if information is relevant, an item should not be recognized if doing so does not provide a faithful representation. A key factor here is measurement uncertainty. If the level of uncertainty is so high that a reasonable estimate cannot be made, recognition could mislead users. In such cases, a different, perhaps less relevant but more reliable measure might be selected, or the element might not be recognized at all.

6.2. Principles of Derecognition

Derecognition is the removal of all or part of a recognized asset or liability from an entity’s statement of financial position (paragraph 5.26).

The main aim of derecognition requirements is to faithfully represent both the assets and liabilities retained and the changes in the entity’s financial position as a result of the transaction (paragraph 5.27).

Derecognition is appropriate under the following conditions:

- For an asset: When the entity loses control of all or part of the recognized asset (e.g., upon sale).

- For a liability: When the entity no longer has a present obligation for all or part of the recognized liability (e.g., when the obligation is discharged, cancelled, or expires).

After deciding to recognize an element, the next step is determining its monetary value—its measurement.

7. Measurement of Elements of Financial Statements

Measurement is the process of quantifying, in monetary terms, the elements of financial statements that are recognized in the statement of financial position and statement of financial performance. The selection of a measurement basis is critical, as it directly affects the information provided to users and their subsequent economic decisions.

7.1. Measurement Bases

The Conceptual Framework categorizes measurement bases into two main types: historical cost and current value.

- Historical cost: This measurement is derived from the price of the transaction or other event that gave rise to the element. The historical cost of an asset comprises the costs incurred in acquiring or creating the asset. Over time, it is updated to depict the consumption (depreciation/amortization), impairment, or repayment of the asset (paragraphs 6.4–6.9).

- Current value: This measurement provides information updated to reflect conditions at the measurement date. It is not derived from the price of the initial transaction. The main types of current value include (paragraphs 6.10–6.22):

- Fair value: The price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date.

- Value in use (for assets) and fulfillment value (for liabilities): The present value of the cash flows, or other economic benefits, that an entity expects to derive from the use of an asset and from its ultimate disposal, or expects to be obliged to transfer as it fulfils a liability.

- Current cost: The cost of an equivalent asset at the measurement date, comprising the consideration that would be paid at the measurement date plus the transaction costs that would be incurred at that date.

7.2. Selection of a Measurement Basis

Selecting a measurement basis is a complex decision that requires considering a range of factors to ensure the provision of the most useful information (paragraphs 6.43–6.63). Key selection criteria include:

- Relevance: The choice depends on the characteristics of the asset or liability (e.g., sensitivity to market fluctuations) and how the item contributes to future cash flows. For assets with volatile values, current value may be more relevant than historical cost.

- Faithful representation: Measurement uncertainty must be considered. If a current value estimate is subject to significant measurement uncertainty, it may not provide a faithful representation. It is also crucial to avoid accounting mismatch, where related assets and liabilities are measured on different bases, potentially distorting financial performance.

- Enhancing qualitative characteristics and the cost constraint: The selected basis should enhance comparability, verifiability, and understandability, and the benefits of using it must outweigh the costs.

The following tables, based on Table 6.1 of the Conceptual Framework, summarize the information provided by different measurement bases for assets.

Table 7.1: Summary of Information Provided by Measurement Bases (Assets)

| Historical Cost | Fair Value (Market Participant Assumptions) | Value in Use (Entity-Specific Assumptions) (a) | Current Cost | |

|---|---|---|---|---|

| Statement of Financial Position | ||||

| Carrying Amount | Historical cost (including transaction costs), unconsumed and recoverable portion. | Price that would be received to sell the asset (excluding transaction costs on disposal). | Present value of future cash flows from use and disposal (net of transaction costs on disposal). | Current cost (including transaction costs), unconsumed and recoverable portion. |

| Statement(s) of Financial Performance | ||||

| Event | Historical Cost | Fair Value (Market Participant Assumptions) | Fulfillment Value (Entity-Specific Assumptions) (a) | Current Cost |

| Initial Recognition(b) | – | Difference between consideration paid and fair value of the asset acquired (b) | Difference between consideration paid and value in use of the asset acquired. | – |

| Sale or Consumption(d), (e) | Expense equal to historical cost. Income received. | Expense equal to fair value. Income received. Transaction costs on sale. | Expense equal to value in use. Income received. Transaction costs on sale. | Expense equal to current cost. Income received. Transaction costs on sale. |

| Interest Income | Interest income at historical rates. | Reflected in changes in fair value. | Reflected in changes in value in use. (May be identified separately). | Interest income at current rates. (May be identified separately). |

| Impairment | Expense arising because historical cost is no longer recoverable. | Reflected in changes in fair value. | Reflected in changes in value in use. (May be identified separately). | Expense arising because current cost is no longer recoverable. |

| Changes in Value | Not recognized (except for impairment). For financial assets—changes in expected cash flows. | Reflected in income and expenses from changes in fair value. | Reflected in income and expenses from changes in value in use. | Income and expenses reflect the effect of price changes (holding gains/losses). |

(a) This column summarizes the information provided if value in use is used as a measurement basis. However, as noted in paragraph 6.75, value in use may not be a practical measurement basis for regular remeasurement.

(b) Income or expenses may arise on initial recognition of an asset not acquired on market terms.

(с) Income or expenses may arise if the market in which the asset is acquired is different from the market that is the source of the prices used when measuring the fair value of the asset.

(d) Consumption of the asset is typically reported through cost of sales, depreciation, or amortization.

(e) Income received is often equal to the consideration received, but will depend on the measurement basis used for any related liability.

Table 7.2: Summary of Information Provided by Measurement Bases (Liabilities)

| Historical Cost | Fair Value (Market Participant Assumptions) | Fulfillment Value (Entity-Specific Assumptions) | Current Cost | |

|---|---|---|---|---|

| Statement of Financial Position | ||||

| Carrying Amount | Consideration received (net of transaction costs) for the unfulfilled part, increased if the liability is onerous. (Accrued interest). | Price that would be paid to transfer the unfulfilled part (excluding transaction costs). | Present value of future cash flows to fulfill the unfulfilled part (including transaction costs). | Consideration that would be received now (net of transaction costs), increased if the liability is onerous. |

| Statement(s) of Financial Performance | ||||

| Event | Historical Cost | Fair Value (Market Participant Assumptions) | Fulfillment Value (Entity-Specific Assumptions) | Current Cost |

| Initial Recognition(a) | — | Difference between consideration received and fair value of the liability (b) | Difference between consideration received and fulfillment value of the liability. | — |

| Fulfillment / Transfer | Income equal to historical cost. Expenses incurred in fulfillment/transfer. | Income equal to fair value. Expenses incurred in fulfillment/transfer. | Income equal to fulfillment value. Expenses incurred in fulfillment/transfer. | Income equal to current cost. Expenses incurred in fulfillment/transfer. |

| Interest Expenses | Interest expenses at historical rates. | Reflected in changes in fair value. | Reflected in changes in fulfillment value. (May be identified separately). | Interest expenses at current rates. (May be identified separately). |

| Effect of Onerousness | Expense equal to the excess of expected outflows over historical cost. | Reflected in changes in fair value. | Reflected in changes in fulfillment value. (May be identified separately). | Expense equal to the excess of expected outflows over current cost. |

| Changes in Value | Not recognized (except for onerousness). For financial liabilities—changes in expected cash flows. | Reflected in income and expenses from changes in fair value. | Reflected in income and expenses from changes in fulfillment value. | Income and expenses reflect the effect of price changes (holding gains/losses). |

(a) Income or expenses may arise on initial recognition of a liability incurred or taken on terms different from market terms.

(b) Income or expenses may arise if the market in which the liability is incurred or taken on is different from the market that is the source of the prices used when measuring the fair value of the liability.

Thus, the correct selection of a measurement basis is always a trade-off between relevance, faithful representation, and practical constraints, aimed at providing users with the most useful and balanced financial information.