Why CFOs and Supervisory Board Members Must Prepare for the New Era of Corporate Reporting Today

Introduction: The Evolution of Corporate Reporting: From Figures to a Holistic Vision

As a CFO with many years of experience, I have frequently observed investors and regulators asking questions that extend far beyond traditional financial metrics. “How does your ESG strategy impact financial results?”, “What role does human capital play in your business model?”, “How might climate risks affect future profitability?”—these questions are becoming the norm, not the exception.

Integrated Reporting (IR) is not merely another trend, but a natural response to these challenges. It represents the next stage in the evolution of corporate communication, where financial and non-financial metrics converge into a single, cohesive narrative about value creation.

What is Integrated Reporting?

An integrated report is a concise communication about how an organization’s strategy, governance, performance, and prospects, in the context of its external environment, lead to the creation, preservation, or erosion of value over the short, medium, and long term.

It is not simply the sum of different reports—such as financial statements and sustainability reports—but rather their deep integration. The goal is to clearly demonstrate the connectivity of information to communicate how value is created, preserved, or lost over time, forming a holistic and coherent picture.

The specific emphasis on conciseness—despite the broad scope covering factors like strategy, governance, performance, prospects, and the external environment—underscores the key task of integrated reporting: transforming complex interdependencies into information that is easily digestible and useful for decision-making. This requires organizations implementing IR to develop strong analytical and communication capabilities to synthesize large volumes of data into a coherent narrative, shifting from simple disclosure to an effective presentation of the business’s essence.

Key Concepts: Integrated Thinking and Its Role

Integrated reporting is the result of a process based on Integrated Thinking. Integrated thinking is the active consideration by an organization of the relationships between its various operating and functional units and the capitals that the organization uses or affects.

This approach promotes integrated decision-making and actions that consider the creation, preservation, or erosion of value over the short, medium, and long term.

Integrated thinking serves as the internal engine that drives effective integrated reporting. It is not merely an external reporting activity, but an internal transformation of how an organization perceives its resources, operations, and their impact. The true, deeper value of integrated reporting lies not only in the report itself but in the internal processes and mindset shifts it stimulates. This leads to better strategic alignment, more holistic risk management, and, ultimately, a more resilient and future-oriented business model. The more integrated thinking is embedded into an organization’s activities, the more naturally the connectivity of information will manifest in management reporting, analysis, and decision-making.

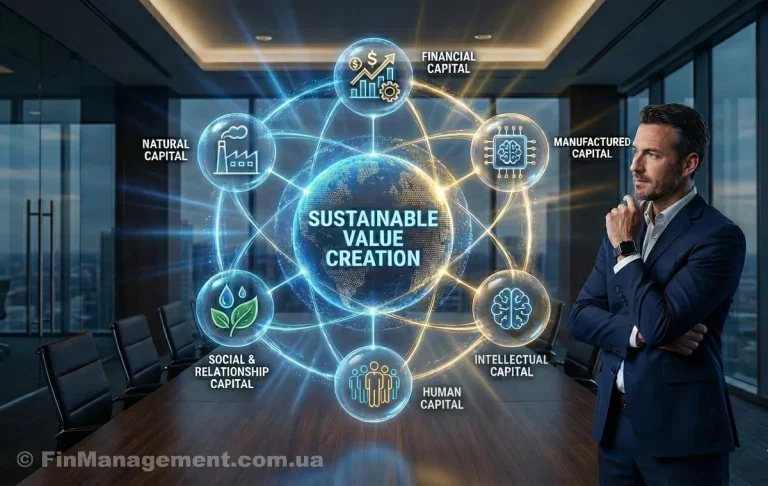

The Six Capitals as the Foundation for Understanding Value

Traditional reporting focuses predominantly on financial capital. Integrated Reporting recognizes that value is created through the interaction of six capitals:

- Financial Capital – The pool of funds available to an organization (the traditional foundation).

It ensures liquidity, solvency, and investment opportunities, serving as the basis for all other activities and value creation. - Manufactured Capital – Physical assets and infrastructure.

It enables production processes and ensures operational efficiency and business scalability. - Intellectual Capital – Knowledge, patents, systems, and processes.

It drives innovation, competitive advantages, process efficiency, and the development of new products/services. - Human Capital – Employee skills, experience, and motivation.

It determines the organization’s ability to innovate, adapt, manage effectively, and execute strategy, directly influencing productivity and quality. - Social and Relationship Capital – Relationships with stakeholders and reputation.

It builds trust, collaboration, and customer and employee loyalty, while also securing a “social license to operate,” thereby reducing risks and unlocking new opportunities. - Natural Capital – Natural resources and processes.

It provides the source of raw materials, energy, and essential ecosystem services critical for long-term operational resilience and the minimization of environmental risks.

This model allows management and investors to understand the real drivers of the company’s long-term value.

Objectives and Purpose of Integrated Reporting

Integrated Reporting aims to achieve several key objectives that extend beyond traditional forms of corporate reporting.

Improving the Quality of Information for Providers of Financial Capital

The primary purpose of an integrated report is to explain to providers of financial capital how an organization creates, preserves, or erodes value over time.

By providing higher quality and more comprehensive information, <IR> promotes a more efficient and productive allocation of capital in the market, directing investment toward companies capable of creating sustainable value.

The focus on providers of financial capital indicates that, despite the broad coverage of non-financial capitals, Integrated Reporting is fundamentally designed to serve the investment community. This means that non-financial information included in the report is considered financially material, bridging the gap between traditional financial analysis and broader sustainability considerations, thereby enabling more informed investment decisions.

Promoting a Cohesive and Efficient Approach to Corporate Reporting

Integrated Reporting seeks to move away from siloed and static reports, creating a holistic picture of the interconnections between various factors affecting value creation.

This is achieved by applying the principle of connectivity of information, which highlights the interdependencies between content elements, the past, present, and future, as well as between financial and other information.

Such an approach helps avoid information fragmentation and ensures a more comprehensive understanding of the organization’s activities.

Enhancing Accountability and Stewardship of Capitals

<IR> raises the level of accountability and responsible stewardship regarding all six capitals, promoting an understanding of their interdependencies.

This includes disclosing how the organization understands, considers, and responds to the legitimate needs and interests of key stakeholders.

By extending accountability beyond solely financial capital to include manufactured, intellectual, human, social and relationship, and natural capitals, Integrated Reporting fundamentally reevaluates corporate governance. This implies a shift toward a more responsible and sustainable business model, where long-term value creation is inextricably linked to the careful stewardship of all resources—even those not traditionally owned or controlled by the company (e.g., natural capital or the social license to operate). This broader accountability facilitates a more holistic approach to risk management and opportunity identification.

Facilitating Integrated Decision-Making and Actions

Integrated Reporting actively supports integrated thinking, leading to more effective decision-making and actions focused on value creation over the short, medium, and long term.

This means decisions are made considering all interconnections and trade-offs between different capitals and time horizons, allowing management to optimize resource use for the business’s long-term success and resilience.

Benefits of Integrated Reporting for Organizations and Investors

Adopting Integrated Reporting delivers significant benefits to both organizations and providers of financial capital, contributing to a more resilient and transparent corporate environment.

For Organizations:

- Improving Strategic Planning and Decision-Making: The Integrated Thinking underpinning <IR> compels management to analyze the interconnections between value creation factors more deeply. This leads to more informed and forward-looking strategic decisions that account for both financial and non-financial risks and opportunities.

Internal adoption of integrated thinking, driven by the need to prepare an integrated report, acts as a powerful catalyst for organizational learning and adaptation. This internal benefit, often underestimated, can be more significant than the external reporting itself, resulting in a more resilient and future-proof business model that anticipates and responds effectively to complex challenges.

- Enhancing Operational Efficiency: A deeper understanding of capital usage and their interdependencies helps optimize internal processes, identify inefficiencies, and reduce operational risks, leading to a more rational allocation of resources and improved overall productivity.

- Strengthening Reputation and Trust: Transparency regarding the stewardship of all capitals, including social and natural, builds trust among all stakeholders—customers, employees, suppliers, local communities, and regulators. This directly strengthens the company’s “social and relationship capital.”

Building social and relationship capital through transparent integrated reporting can reinforce the “social license to operate,” which is becoming increasingly critical in an ESG-sensitive world. This translates directly into reduced regulatory risks, higher brand loyalty, improved access to talent, and potentially more favorable terms with business partners, demonstrating the ripple effect from reporting to operational stability and competitive advantage.

- Attracting Capital: Providing high-quality, holistic information on value creation makes the company more attractive to investors focused on the long term and sustainability, as they gain a more complete picture of risks and opportunities, as well as an understanding of long-term growth potential.

For Investors (Providers of Financial Capital):

- Deeper Understanding of Business Model and Risks: Integrated Reporting gives investors a comprehensive view of how an organization creates value, including non-financial factors and their impact on future financial performance. This allows them to better assess long-term potential and risks, moving beyond short-term financial metrics.

- Efficient Capital Allocation: Access to higher quality and connected information enables investors to make more informed decisions about where to direct their capital, facilitating a more productive and responsible allocation of capital in the market.

- Assessing Long-Term Sustainability: <IR> allows investors to evaluate not just current financial performance, but the company’s ability to create value over the long term, considering its stewardship of all capitals and response to the external environment. This is critical for long-term investment decisions.

For investors, Integrated Reporting significantly reduces information asymmetry, enabling a more accurate and comprehensive valuation of the enterprise. This shifts the investment focus from short-term financial gains to sustainable, viable business models, potentially influencing capital markets toward more responsible and long-term oriented investments. It can also lead to a lower cost of capital for companies effectively implementing <IR> due to reduced perceived risk.

Institutional Support: Regulation and Mandating of Integrated Reporting

A landmark event occurred in August 2022: the IFRS Foundation consolidated the Value Reporting Foundation, assuming direct responsibility for the development of the International <IR> Framework 1.

This is not merely an administrative decision. The International Accounting Standards Board (IASB) and the International Sustainability Standards Board (ISSB) now share responsibility for Integrated Reporting, signifying its integration into the mainstream of global financial reporting.

Mandatory Status: Not “If,” But “When”

There are other initiatives and frameworks that complement or facilitate Integrated Reporting:

- The Prince’s Accounting for Sustainability Project (A4S) offers reporting frameworks that incorporate ESG issues.

- WICI (World Intellectual Capital Initiative) seeks to develop a voluntary global framework for measuring and reporting corporate performance.

- The EU Corporate Sustainability Reporting Directive (CSRD) (Directive 2022/2464/EU) includes requirements for a partial description of the business model, which aligns with the principles of the International <IR> Framework.

While Integrated Reporting is not yet universally mandatory, trends indicate the inevitability of this step.

Examples of Mandatory or Partially Mandatory Use:

- Brazil: The Securities Commission (CVM) has mandated that public companies prepare integrated reports in accordance with the International Framework 2.

- EU: The Corporate Sustainability Reporting Directive (CSRD) contains requirements for describing the business model consistent with <IR> principles 3.

- Ukraine: The first integrated report regarding the National Energy and Climate Plan has already been submitted to the Energy Community in accordance with EU Regulation 2018/1999 4.

This demonstrates the mandatory nature of Integrated Reporting in specific sectors, particularly in energy and climate policy, for the purposes of European integration.

Although Integrated Reporting remains voluntary for many companies, growing pressure from investors, regulators, and society, combined with the integration of the <IR> Framework into the IFRS Foundation structure, points to a clear movement toward its broader and potentially mandatory application in the future.

Projected Timeline:

- 2025–2026: Preparatory period, development of methodological guidelines.

- 2027–2028: Probable introduction of mandatory requirements for large enterprises.

- 2029+: Expansion to medium-sized enterprises.

Challenges in Implementing <IR> and Ways to Overcome Them

The biggest obstacles to implementing <IR> are:

- Complexity of Data Integration: Requires investment in IT systems and processes.

- Need for Cultural Change: A shift from “silo mentality” to an integrated approach.

- Lack of Expertise: The need to train teams and engage consultants.

Recommendation: Start small, focusing on the capitals that are most material to your business.

The Role of the Supervisory Board and the CFO

I believe the role of the Supervisory Board consists of:

- Ensuring a strategic vision for long-term value creation.

- Overseeing the quality of integrated reporting and its compliance with international standards.

- Promoting the development of integrated thinking at all levels of the organization.

CFOs must become “translators” between financial and non-financial metrics, demonstrating their mutual impact on value creation.

Conclusions and Recommendations

Integrated Reporting is not just a new document format, but a transformation of business thinking. Companies that begin implementation today will gain significant competitive advantages:

- Start with Analysis: Determine which capitals most significantly impact your business model.

- Invest in Data Collection and Analysis Systems: This is the foundation of quality integrated reporting.

- Develop Team Competencies: Conduct training on integrated thinking.

- Engage Stakeholders: Their understanding and support are critical for success.

We stand on the cusp of a new era of corporate transparency. The question is not whether Integrated Reporting will come to Ukraine, but how ready we will be for it.

Sources:

- IFRS Foundation consolidates Value Reporting Foundation, August 2022. ↩

- Brazil Securities Commission (CVM) Instruction 586/2017. ↩

- EU Corporate Sustainability Reporting Directive (CSRD) 2022/2464/EU. ↩

- EU Regulation 2018/1999 on the Governance of the Energy Union and Climate Action. ↩

Useful Resources:

- International Integrated Reporting Framework: www.integratedreporting.org

- IFRS Sustainability Standards: www.ifrs.org

- New Sustainability Disclosure Standards IFRS S1 and IFRS S2

- Law of Ukraine “On Accounting and Financial Reporting” No. 996-XIV